SMM, February 5: After the Chinese New Year holiday, SHFE lead resumed trading on February 5 (the eighth day of the lunar calendar). At the opening, SHFE lead surged strongly, breaking through the 5-day and 40-day moving averages consecutively, reaching a one-month high of 17,110 yuan/mt. By the close at 15:00, the most-traded SHFE lead contract settled at 17,095 yuan/mt, up 390 yuan/mt or 2.33%.

》Check SMM Lead Spot Quotations

During the Chinese New Year holiday, the domestic market was closed, while the overseas market operated as usual. Notably, significant changes occurred in the US-China tariff policies during this period. On February 1, 2025, the US government announced a 10% tariff hike on all Chinese goods exported to the US, citing issues such as fentanyl. On February 4, 2025, China's State Council Tariff Commission issued a notice stating that, with State Council approval, tariffs on certain US-origin imports would be raised starting February 10, 2025. Specifically, a 15% tariff will be imposed on coal and liquefied natural gas, while a 10% tariff will be applied to crude oil, agricultural machinery, large-displacement vehicles, and pickup trucks. These tariff increases on energy products may indirectly raise lead smelting costs, while the automotive tariffs could shift consumption to the domestic market. The US tariff hike on all Chinese goods exported to the US also impacts the lead industry chain. For instance, in 2024, China exported 8.3 million lead-acid batteries to the US, accounting for 3.3% of China's total lead-acid battery exports.

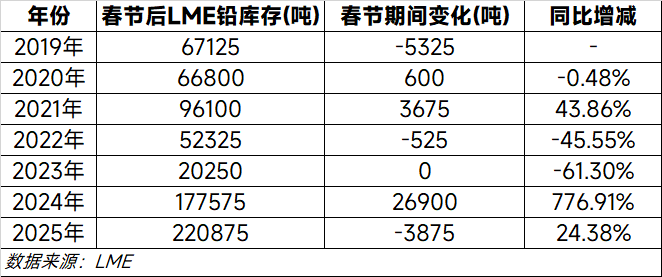

From the perspective of lead fundamentals, overseas lead ingot inventories declined YoY during the Chinese New Year holiday. As of February 4, LME lead inventory stood at 220,875 mt, although the inventory base increased compared to 2024, the inventory decreased by 3,875 mt during the holiday. Domestically, SHFE lead warehouse warrant inventory on February 5 was 30,329 mt, up 181 mt from January 27. The chart below shows LME lead inventory changes during the Chinese New Year over the past seven years:

》Click to View SMM Historical Spot Prices

Additionally, it is understood that during the Chinese New Year holiday, domestic lead smelters had minimal shutdowns, especially large and medium-sized primary lead smelters, which mostly maintained normal production. Coupled with the suspension of logistics during the holiday, lead ingot shipments were halted, leading to a general increase in in-plant inventory at smelters after the holiday, with an estimated inventory buildup of 40,000-50,000 mt. In contrast to the inventory buildup of primary lead, secondary lead smelters saw a YoY decline in lead ingot inventory buildup during the holiday. This was mainly because fewer large and medium-sized secondary lead smelters operated during this year's Chinese New Year period. For example, in Anhui, the largest production area, half of the secondary lead smelters were either on holiday or undergoing maintenance.

According to the holiday schedules of lead-acid battery enterprises, the majority planned to resume operations on February 4-5, with some starting on February 7-9, and production is expected to return to normal around the Lantern Festival (February 12). Currently, downstream lead-acid battery enterprises are gradually resuming production. Since most had sufficient lead ingot inventory to ensure production before the holiday, downstream enterprises adopted a wait-and-see approach following the rise in lead prices. On February 5, the lead spot market saw only tentative quotations from suppliers. For instance, mainstream regions quoted primary lead ex-factory prices at premiums of 0-100 yuan/mt against the SMM 1# lead average price, but actual transactions were minimal.

In summary, in the short term, as lead consumption has not fully recovered, the destocking of lead ingots accumulated during the Chinese New Year holiday is progressing slowly. This is primarily a process of transferring inventory from in-plant to social warehouses as logistics resume. Moving forward, attention should be paid to whether the timing of secondary lead smelters resuming production and supplying goods aligns with downstream enterprises' post-holiday restocking.